As we settle into the middle of Q1 2026, the marketplace landscape is moving faster than ever. For Amazon and Walmart brands, now is the critical window where Q4 2025 performance data transitions from retroactive reporting into proactive advertising strategies for the rest of the year.

Following Amazon’s recently released Q4 2025 earnings report—which we explored in a previous article outlining the broader revenue drivers impacting marketplace sellers—we are now looking at the tactical advertising metrics that dictated Q4 success.

To give our clients the clearest picture possible, Brandwoven’s team has analyzed the newly released Q4 2025 Retail Media Benchmark Report from our valued partners at Pacvue and Helium10. For context, Brandwoven relies heavily on Pacvue’s advanced marketing dashboarding, reporting, and campaign management technology to drive our omni-channel advertising strategies for Amazon and Walmart, while we utilize Helium10’s robust tools for keyword research and market share analyses.

By layering Pacvue’s extensive platform-wide data over our own internal client performance observations, our marketing managers have identified critical shifts in how Cost-Per-Click (CPC), ad placements, and format types are dictating Return on Ad Spend (ROAS). Below, we break down our team’s top takeaways from Q4 and explain how brands must adapt their Amazon and Walmart advertising strategies for 2026.

The Big Picture: Audience Relevance Over Aggressive Bidding

Before diving into specific ad types, it is important to understand the overarching theme of Q4 2025: the market rewarded relevance and conversion quality over brute-force bidding. Across Amazon, Walmart, Target, and Instacart, the strongest performance gains came from brands that aligned closely with shopper intent. As we noted in our Cyber 5 recap, Q4 was not about capturing a flood of casual browsers, but about winning the battle for high-intent shoppers who already knew what they wanted.

However, underneath these high-level efficiency gains, our Brandwoven marketing managers noticed significant structural changes to how ad placements are performing on the ground—starting with the inflation of standard search placements.

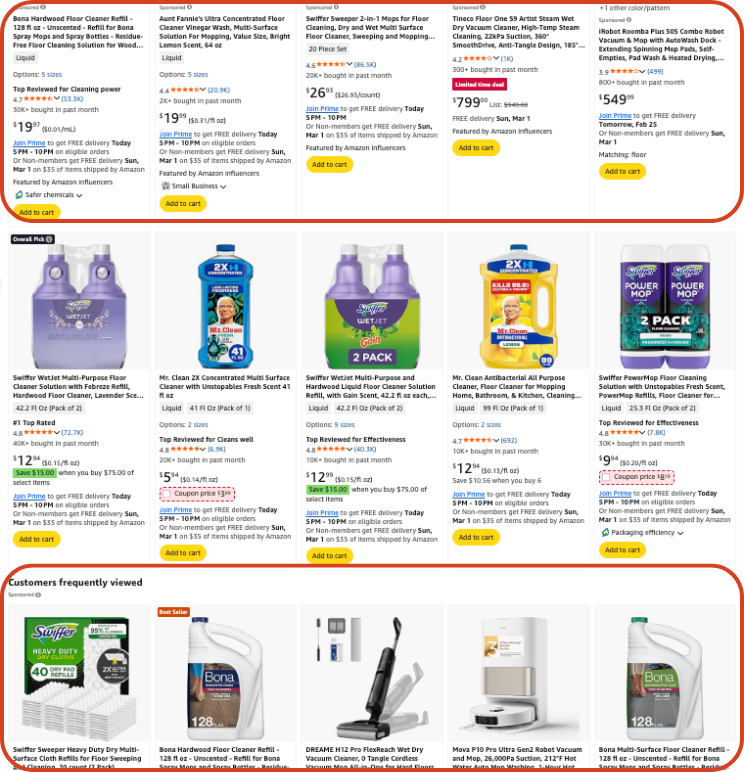

Takeaway 1: Rising Ad Load

When reviewing the Q4 data, one of the most glaring trends observed by our marketing team is the stagnation of Sponsored Products (SP) CPC alongside a paradoxically sharp rise in daily spend. In Q4, Amazon Sponsored Products average daily ad spend increased by 11.6% quarter-over-quarter, yet CPC slightly declined by -0.8%. At the same time, many categories experienced a drop in Conversion Rate (CVR).

How can spend increase drastically while clicks cost the same and convert less? Rising ad load.

As our Marketing Manager pointed out, we saw a YoY drop in traffic during the Turkey 12 (T12) period for several of our clients’ markets. For example, traffic for our thermal imaging brand was down 48% YoY. To maintain and grow advertising revenue in a traffic-constrained environment, Amazon flooded product detail pages and search results with an increasing number of ad placements.

Because there are simply more places for an ad to appear, SP campaigns are becoming “watered down.” If your campaigns are not highly dialed in with strict placement modifiers, Amazon will ensure your ads serve somewhere—often in lower-converting, bottom-of-page, or obscure detail page locations—just to access your ad dollars. This means brands can no longer rely on broad SP campaigns; success in 2026 requires meticulous bid management to ensure your budget is actually securing premium, high-converting real estate.

Takeaway 2: Top-of-Search Amazon Advertising Videos

With Sponsored Products feeling the effects of Amazon ad placement inflation, Sponsored Brands (SB) ads emerged as the primary performance lever of Q4 2025. This is the most crucial takeaway for brands planning their 2026 budgets.

Across the Pacvue data, Sponsored Brand ads delivered incredible efficiency improvements, with ROAS almost reaching parity with Sponsored Products (and actually surpassing it during the Cyber 5 peak). Furthermore, our internal data shows that while SP campaigns were watered down, Sponsored Brand campaigns did not see an overall increase in CPC and consistently grew more efficient.

The driving force behind this efficiency is Amazon Sponsored Brand Video (SBV) placements at Top-of-Search. As Pacvue’s President Melissa Burdick rightly stated within the report, “video can no longer be treated as a nice-to-have”; it is non-negotiable.

Historically, Amazon video ads were limited to below-the-fold placements, but Q4 2025 represented the first full quarter where SBV expanded to occupy premium Top-of-Search real estate. These massive video ads, which take up nearly half the screen on a mobile device, proved to be extremely valuable in driving sales for our clients during peak Q4 events like Amazon Prime Big Deal Days. Across the board, Click-Through Rates (CTR), CVR, and ROAS have been substantially higher for these video ads compared to basic static image ads.

Balancing Amazon Brand Value & Advertising ROI

If Amazon Top-of-Search video advertising is so dominant, why did the Pacvue report show that overall Sponsored Brand CPC barely moved (up just 0.6% QoQ)?

Here lies the strategic nuance: A video ad at the very top of the page on a perfect, high-traffic keyword is extraordinarily expensive. Our marketing managers observed CPCs soaring up to $15-20 for highly competitive Top-of-Search SBV placements for our CPG clients (in one example, a beverage product that retails for only ~$36). In cases like these, paying $20 for a single click to a product page severely challenges traditional ROAS goals.

However, this astronomical cost is being evened out in the aggregate data by the sheer inflation of other ad placements. Because Amazon has exponentially increased the number of SB and SBV locations across detail pages and rest-of-search locations (which carry a much lower cost), the average CPC appears flat.

This dynamic completely changes how we evaluate Amazon brand value and advertising ROI. Securing that $20 Top-of-Search video click isn’t just about the immediate ROAS of that single transaction; it is a defensive and offensive branding maneuver. These dominant mobile placements ensure maximum share-of-voice, push competitors entirely off the screen, and drive New-to-Brand (NTB) customer acquisition.

To make the most out of marketplace advertising investment, brands cannot look at CPC in a vacuum. Instead:

- Leverage Amazon Marketing Cloud (AMC) and Pacvue’s dayparting and bid modifier tools

- Willingly pay the premium price of Top-of-Search video advertising

- Focus on the highest-converting, most valuable keywords

- Strictly control bids on rest-of-search placements

This blend in your overall campaign strategy will lead to a respectable ROAS and profitable margin.

Takeaway 3: The Impact of Walmart’s Minimum Advertising Bid Drop

During Q4 2025, Walmart dropped its minimum required bid for Sponsored Brand ads from $1.00 down to $0.50.

Interestingly, Walmart’s backend literature and certification tests still state the minimum bid is $1.00, creating confusion for brands not actively creating new campaigns.

Our marketing team immediately capitalized on this change. The direct result of halving the bid floor was a massive drop in CPC, with Walmart Connect CPC plunging -30.1% YoY. However, this didn’t lead to brands pocketing the savings. Instead, overall average daily spend for Sponsored Brand ads on Walmart skyrocketed (+16.2% QoQ). With CPCs lower and spend up for the quarter, this led to a +36.4% YoY increase in ROAS for brands advertising on Walmart marketplace.

With this in mind, brands moving onto Walmart marketplace or those already selling online can see that the barrier to entry for Sponsored Brands has been lowered.

You can now stretch your Walmart ad dollars much further, but you must actively monitor your CPCs to ensure you are taking advantage of the new $0.50 floor rather than blindly overpaying based on outdated platform minimums.

Conclusion: Use Data Analysis to Optimize Ad Performance

The Pacvue and Helium10 Q4 Benchmark Report confirms what our Brandwoven marketing team sees every day: marketplace advertising is not a set-it-and-forget-it landscape. The days of relying solely on broad Sponsored Products ad campaigns to drive top-line revenue are over.

To maximize ad spend and boost CVR, brands must adopt a highly intentional ad placement strategy:

- Utilize advanced bid modifiers to aggressively target Top-of-Search placements

- Invest in high-quality video creative to win Sponsored Brands mobile real estate on Amazon

- Regularly monitor platform changes (like Walmart’s bid floors) to maintain efficiency

Improve Your Advertising ROI with Brandwoven

Navigating ad placement inflation, high video CPCs, and complex bid modifiers requires deep marketplace expertise and elite technology. At Brandwoven, we combine our Amazon and Walmart advertising expertise with industry-leading tools like Pacvue and Helium10 to ensure your budget is focused where it matters most: premium placements and high-value audiences.

Whether you need to optimize your Amazon bidding strategy, overhaul your creative for Sponsored Brand Video, or scale your presence on Walmart Connect, our team is ready to help you dominate your category with a strategic and agile approach to advertising.